A 1. Under job order cost accumulation, the factory overhead control account controls:

A. factory overhead analysis sheets

B. all general ledger subsidiary accounts

C. job order cost sheets

D. cost reports by processes

E. materials inventories

B 2. Supplies needed for use in the factory are issued on the basis of:

A. job cost sheets

B. materials requisitions

C. time tickets

D. factory overhead analysis sheets

E. clock cards

B 3. Finished Goods is debited and Work in Process is credited for a:

A. transfer of completed goods out of the factory

B. transfer of completed production to the finished goods storeroom

C. purchase of goods on account

D. transfer of materials to the factory

E. return of unused materials from the factory

A 4. In job order costing, when materials are returned to the storekeeper that were previously issued to the factory for cleaning supplies, the journal entry should be made to:

A. Materials

Factory Overhead

B. Materials

Work in Process

C. Purchases Returns

Work in Process

D. Work in Process

Materials

E. Factory Overhead

Work in Process

A 5. Under a job order cost system, the dollar amount of the entry to transfer the inventory from Work in Process to Finished Goods is the sum of the costs charged to all jobs:

A. completed during the period

B. started in process during the period

C. in process during the period

D. completed and sold during the period

E. none of the above

B 6. When a manufacturing company has a highly automated plant producing many different products, probably the most appropriate basis of applying factory overhead costs to Work in Process is:

A. units processed

B. machine hours

C. direct labor hours

D. direct labor dollars

E. none of the above

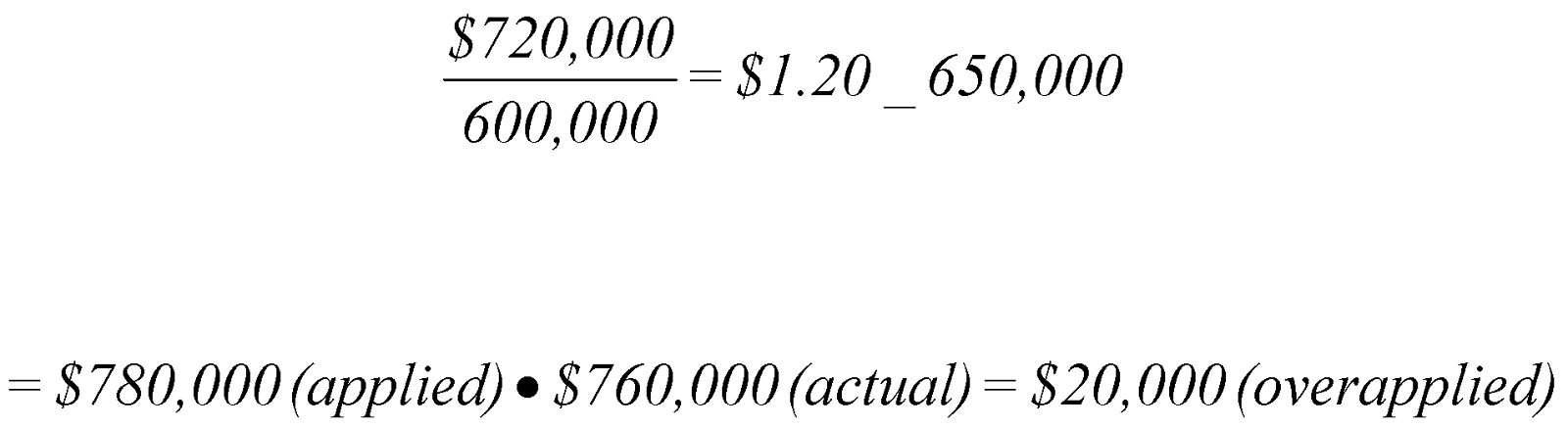

A 7. Cherokee Company applies factory overhead on the basis of direct labor hours. Budget and actual data for direct labor and overhead for the year are as follows:

Budget Actual

Direct labor hours 600,000 650,000

Factory overhead costs $720,000 $760,000

The factory overhead for Cherokee for the year is:

A. overapplied by $20,000

B. overapplied by $40,000

C. underapplied by $20,000

D. underapplied by $40,000

E. neither underapplied nor overapplied

SUPPORTING CALCULATION:

C 8. At the end of the year, Paola Company had the following account balances after applied factory overhead had been closed to Factory Overhead Control:

Factory Overhead Control $ 1,000 CR

Cost of Goods Sold 980,000 DR

Work in Process 38,000 DR

Finished Goods 82,000 DR

The most common treatment of the balance in Factory Overhead Control would be to:

A. carry it as a deferred credit on the balance sheet

B. report it as miscellaneous operating revenue on the income statement

C. credit it to Cost of Goods Sold

D. prorate it between Work in Process and Finished Goods

E. prorate it among Work in Process, Finished Goods, and Cost of Goods Sold

B 9. Overapplied factory overhead would result if:

A. the plant were operated at less than normal capacity

B. factory overhead costs incurred were less than costs charged to production

C. factory overhead costs incurred were unreasonably large in relation to units produced

D. factory overhead costs incurred were greater than costs charged to production

E. a firm incurred a significant amount of overhead

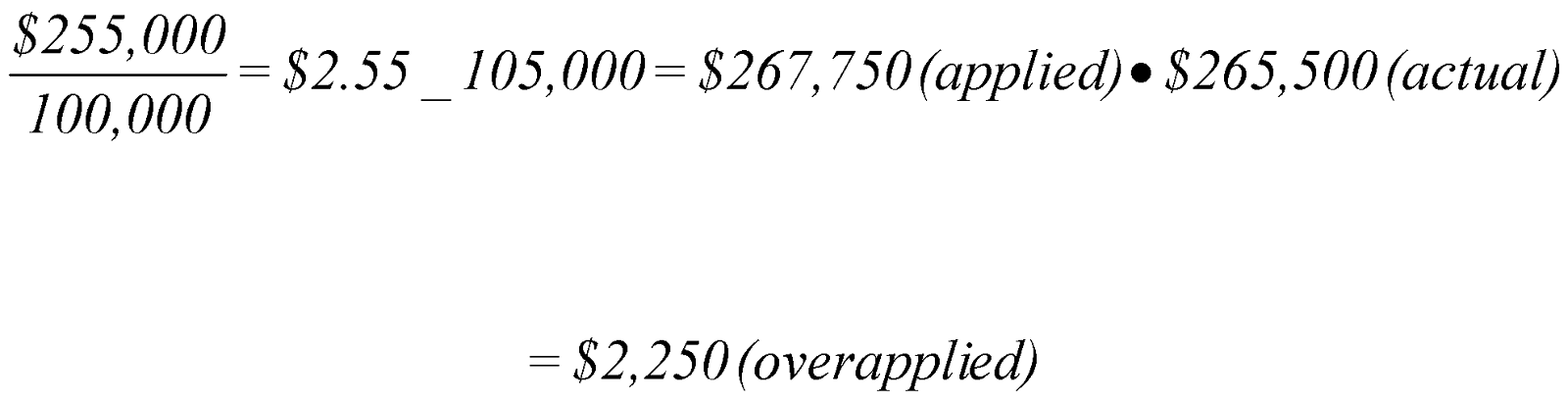

A 10. The Waitkins Company estimated Department A's overhead at $255,000 for the period based on an estimated volume of 100,000 direct labor hours. At the end of the period, the factory overhead control account for Department A had a balance of $265,500; actual direct labor hours were 105,000. What was the over- or under-applied overhead for the period?

A. $2,250

B. $(2,250)

C. $15,000

D. $(15,000)

E. $(5,000)

SUPPORTING CALCULATION:

D 11. Howell Corporation has a job order cost system. The following debits (credits) appeared in Work in Process for the month of July:

July 1, balance $ 12,000

July 31, direct materials 40,000

July 31, direct labor 30,000

July 31, factory overhead 27,000

July 31, to finished goods (100,000)

Howell applies overhead to production at a predetermined rate of 90% based on the direct labor cost. Job 1040, the only job still in process at the end of July, has been charged with factory overhead of $2,250. What was the amount of direct materials charged to Job 1040?

A. $6,750

B. $2,250

C. $2,500

D. $4,250

E. $9,000

SUPPORTING CALCULATION:

Job 1040 = $12,000 + $40,000 + $30,000 + $27,000 - $100,000 = $9,000

E 12. Valentino Corporation makes aluminum fasteners. Among Valentino's 19- manufacturing costs were:

Wages and salaries:

Machine operators $80,000

Factory supervisors 30,000

Machine mechanics 20,000

Direct labor amounted to:

A. $50,000

B. $100,000

C. $110,000

D. $130,000

E. none of the above

B 13. Rudolpho Corporation makes aluminum fasteners. Among Rudolpho's 19-- manufacturing costs were:

Materials and supplies:

Aluminum $400,000

Machine parts 18,000

Lubricants for machines 5,000

Direct materials amounted to:

A. $23,000

B. $400,000

C. $405,000

D. $418,000

E. $423,000

C 14. Selected cost data (in thousands) concerning the past fiscal year's operations of the Moscow Manufacturing Company are presented below.

Inventories

Beginning Ending

Materials $75 $ 85

Work in process 80 30

Finished goods 90 110

Materials used, $326

Total manufacturing costs charged to production during the year (including direct materials, direct labor, and factory overhead applied at the rate of 60% of direct labor cost), $686

Cost of goods available for sale, $826

Selling and general expenses, $25

The cost of direct materials purchased during the year amounted to:

A. $360

B. $316

C. $336

D. $411

E. none of the above

SUPPORTING CALCULATION: $326 + $85 - $75 = $336

C 15. Selected cost data (in thousands) concerning the past fiscal year's operations of the Moscow Manufacturing Company are presented below.

Inventories

Beginning Ending

Materials $75 $ 85

Work in process 80 30

Finished goods 90 110

Materials used, $326

Total manufacturing costs charged to production during the year (including direct materials, direct labor, and factory overhead applied at the rate of 60% of direct labor cost), $686

Cost of goods available for sale, $826

Selling and general expenses, $25

Direct labor costs charged to production during the year amounted to:

A. $216

B. $135

C. $225

D. $360

E. none of the above

SUPPORTING CALCULATION: $686 = $326 + x + .6x

x = $225

A 16. Selected cost data (in thousands) concerning the past fiscal year's operations of the Moscow Manufacturing Company are presented below.

Inventories

Beginning Ending

Materials $75 $ 85

Work in process 80 30

Finished goods 90 110

Materials used, $326

Total manufacturing costs charged to production during the year (including direct materials, direct labor, and factory overhead applied at the rate of 60% of direct labor cost), $686

Cost of goods available for sale, $826

Selling and general expenses, $25

The cost of goods manufactured during the year was:

A. $736

B. $716

C. $636

D. $766

E. none of the above

SUPPORTING CALCULATION: $80 + $686 - $30 = $736

A 17. Selected cost data (in thousands) concerning the past fiscal year's operations of the Moscow Manufacturing Company are presented below.

Inventories

Beginning Ending

Materials $75 $ 85

Work in process 80 30

Finished goods 90 110

Materials used, $326

Total manufacturing costs charged to production during the year (including direct materials, direct labor, and factory overhead applied at the rate of 60% of direct labor cost), $686

Cost of goods available for sale, $826

Selling and general expenses, $25

The cost of goods sold during the year was:

A. $716

B. $691

C. $801

D. $736

E. none of the above

SUPPORTING CALCULATION: $90 + $736 - $110 = $716

A 18. J. D. Doonesbury Company manufactures tools to customer specifications. The following data pertain to Job 1501 for April:

Direct materials used $ 4,200

Direct labor hours worked 300

Direct labor rate per hour $ 8.00

Machine hours used 200

Applied factory overhead rate per machine hour $ 15.00

What is the total manufacturing cost recorded on Job 1501 for April?

A. $9,600

B. $10,300

C. $11,100

D. $5,400

E. $8,800

SUPPORTING CALCULATION: $4,200 + (300 x $8) + (200 x $15) = $9,600

C 19. In service businesses using job order costing, the most commonly used base for applying overhead to jobs is:

A. machine hours

B. direct materials consumed

C. direct labor cost

D. meals, travel, and entertainment

E. none of the above

A 20. In service businesses using job order costing, the hourly rate used to charge costs to a job usually includes:

A. both labor and overhead cost

B. labor cost only

C. overhead cost only

D. labor, overhead, and miscellaneous costs

E. none of the above

A 21. Work in Process is debited and Materials is credited for:

A. the issuance of direct materials into production

B. the issuance of indirect materials into production

C. the return of materials to the storeroom

D. the application of materials overhead

E. none of the above

B 22. Factory Overhead Control is debited and Payroll is credited for:

A. the recording of payroll

B. the distribution of indirect labor costs

C. the distribution of direct labor costs

D. the distribution of withholding taxes

E. none of the above

A 23. Applied Factory Overhead is debited and Factory Overhead is credited to:

A. close the estimated overhead account to actual overhead

B. record the actual factory overhead for the period

C. charge estimated overhead to all jobs worked on during the period

D. to record overapplied overhead for the period

E. none of the above

C 24. The best overhead allocation base to use in a labor-intensive manufacturing environment probably would be:

A. materials cost

B. machine hours

C. direct labor hours

D. units of production

E. none of the above

D 25. Finished Goods is debited and Cost of Goods Sold is credited for:

A. transfer of completed goods to the customer

B. sale of a customer order

C. return of materials to the supplier

D. return of goods by the customer

E. none of the above

PROBLEMS

PROBLEM

1.

Job Order Cost Schedule. Winkel Woodcrafters produces special-order wood products. The company uses job order costing for pricing and cost accumulation purposes. The following costs were incurred on two recent jobs:

Cost Item Job Pine-20 Job Birch-10

Direct materials:

Issued $6,500 $8,000

Returned 500 0

Indirect materials used 500 400

Direct labor $9,000 $15,000

Direct labor rate $9 per hour $10 per hour

Overhead application rate $10 per direct labor hour $15 per direct labor hour

The company adds a 50% markup on cost in determining the amount to charge for each job.

Required: Prepare a schedule showing the cost and the amount to be charged for each job.

SOLUTION

Job Pine20 Job Birch10

Direct materials $ 6,000 $ 8,000

Direct labor 9,000 15,000

Factory overhead applied 10,000 22,500

Total $ 25,000 $ 45,500

Allowance for profit and other costs 12,500 22,750

Amount to be charged $ 37,500 $ 68,250

PROBLEM

2.

Job Order Cost Sheet; Over- or Underapplied Overhead. During June, the following transactions took place at the Cassandran Corp.

June 3 Purchased materials, $30,000.

5 Requisitioned materials from inventory, $20,000 (75% of these were direct; 25% were indirect). Direct materials of $3,000 and indirect materials of $1,000 were for Job 001. The remainder were for Job 002.

7 For Job 002, returned $150 of direct materials and $200 of indirect materials.

8 Recorded liabilities for payroll: direct labor, $15,000 and indirect labor, $5,000. Of the direct labor cost, 60% was for Job 001; the remainder was for Job 002.

10 Incurred other factory overhead costs, $20,000 (all applicable to Jobs 001 and 002).

14 Applied overhead at the rate of 200% of direct labor cost to Jobs 001 and 002, which were completed and transferred to finished goods account today.

Required: Assuming that Jobs 001 and 002 were the only jobs during the period and that all overhead (as recorded above) is the total applicable overhead for these projects:

(1) Prepare a job order cost sheet for each job.

(2) Determine the difference between applied and actual overhead for the month.

SOLUTION

(1)

Job 001 Job 002

Materials $ 3,000 $ 11,850

Labor 9,000 6,000

Overhead applied 18,000 12,000

Total cost $ 30,000 $ 29,850

(2) Analysis of Factory Overhead

Incurred:

Indirect materials $ 4,800

Indirect labor 5,000

Other overhead incurred 20,000 $ 29,800

Applied:

Job 001 $ 18,000

Job 002 12,000 30,000

Amount overapplied $ (200 )

PROBLEM

3.

Job Order Cycle Entries. The following completed cost sheets were prepared for three jobs that were in production during April in the Special Order Division of Byron Company:

Job 097 Job 781 Job 946

Direct materials $ 6,000 $2,700 $4,100

Direct labor 9,200 7,300 8,200

Applied factory overhead 6,900 5,475 6,120

Allowance for commercial expenses and profit 11,050 7,738 9,210

On April 1, Job 097 was 75% complete as to materials, labor, and overhead. It was finished during the month. The other jobs were started and finished during the month. Jobs 097 and 946 were sold on account at the end of the month.

Required: Prepare general journal entries to be recorded in April to accumulate these job costs for Work in Process as well as for Finished Goods and for the sale of the two jobs.

SOLUTION

Debit Credit

Work in Process 8,300 *

Materials 8,300

Work in Process 17,800 **

Accrued Payroll 17,800

Work in Process 13,320 ***

Factory Overhead Control 13,320

Finished Goods 55,995

Work in Process 55,995

Cost of Goods Sold 40,520

Finished Goods 40,520

Accounts Receivable 60,780

Sales 60,780

* (.25 x $6,000) + $2,700 + $4,100

** (.25 x $9,200) + $7,300 + $8,200

*** (.25 x $6,900) + $5,475 + $6,120

PROBLEM

4.

Voyager Inc. produces customized vans in a job order shop. On November 1, the following balances appear in the inventory records:

Finished goods $179,000

Work in process 308,000

Materials 83,000

The amount in Finished Goods represents $101,000 recorded for Van 175 and $78,000 recorded for Van 177. The work in process account represents the three vans in process, as follows:

Van 179 Van 180 Van 181

Factory overhead $75,000 $50,000 $25,000

Direct labor 60,000 40,000 20,000

Direct materials 26,000 7,000 5,000

The following transactions occurred during November:

(a) Purchased materials on account, $80,000.

(b) Requisitioned $60,000 of materials from inventory: $15,000 applied to Van 180, $25,000 to Van 181, and $16,000 to Van 182, a new order; the balance was for indirect materials.

(c) Recorded the liability for the payroll and the labor cost distribution in a single entry: total payroll, $208,750. Of the payroll cost, 10% applied to Van 179, 20% to Van 180, 35% to Van 181, 30% to Van 182, and the remainder to indirect labor.

(d) Paid the payroll.

(e) Applied factory overhead at the rate of 150% of direct labor cost.

(f) Completed Vans 179 and 180.

(g) Sold Vans 175, 177, and 180 at 50% over manufacturing costs.

Required: Prepare general journal entries to record these transactions.

SOLUTION

Debit Credit

(a) Materials 80,000

Accounts Payable 80,000

(b) Factory Overhead Control 4,000

Work in Process 56,000

Materials 60,000

(c) Factory Overhead Control 10,437

Work in Process 198,313

Accrued Payroll 208,750

(d) Accrued Payroll 208,750

Cash 208,750

(e) Work in Process 297,470

Applied Factory Overhead 297,470

(f) Finished Goods 429,563

Work in Process 429,563

(g) Accounts Receivable 593,063

Sales 593,063

Cost of Goods Sold 395,375

Finished Goods 395,375

PROBLEM

5.

Manufacturing Costs. The work in process account of Meyers Company showed:

Work in Process

Materials $22,000 | Finished goods $68,000

Direct labor 37,000 |

Factory overhead 55,500 |

Materials charged to the one job still in process amounted to $5,000. Factory overhead is applied as a predetermined percentage of direct labor cost.

Required: Compute the following:

(1) The amount of direct labor cost in finished goods.

(2) The amount of factory overhead in finished goods.

SOLUTION

(1) The amount of direct labor in finished goods:

Finished goods $68,000

Materials included in finished goods 17,000

Direct labor and factory overhead in finished goods $51,000

Let x = direct labor in finished goods

2.5x = $51,000 direct labor and factory overhead in finished goods

x = $20,400 direct labor in finished goods

(2) The amount of factory overhead in finished goods:

x = $20,400

1.5x = 1.5($20,400)

1.5x = $30,600 factory overhead in finished goods

PROBLEM

6.

Manufacturing Costs. Teddy Company is to submit a bid on the production of 5,500 vases. It is estimated that the cost of materials will be $8,500, and the cost of direct labor will be $12,000. Factory overhead is applied at 50% of direct labor cost in the Molding Department and at $7.50 per direct labor hour in the Finishing Department. Of the above direct labor, it is estimated that 500 direct labor hours at a cost of $4,000 will be required in Finishing. The company wishes a markup of 100% of its total production cost.

Required: Determine the following:

(1) Estimated cost to produce.

(2) Estimated prime cost.

(3) Estimated conversion cost.

(4) Bid price.

SOLUTION

(1) Materials $ 8,500

Direct labor 12,000

Factory overhead:

Molding (50% x $8,000) 4,000

Finishing (500 DLH x $7.50) _ 3,750

Estimated cost to produce $ 28,250

(2) Materials $ 8,500

Direct labor _ 12,000

Estimated prime cost $ 20,500

(3) Direct labor $ 12,000

Factory overhead _ 7,750

Estimated conversion cost $ 19,750

(4) Estimated cost to produce $ 28,250

Markup ($28,250 x 100%) 28,250

Bid price $ 56,500

PROBLEM

7.

Flow of Costs Through T Accounts. The Palmer Company had the following inventories at the beginning and end of July:

July 1 July 31

Materials $20,000 $ 45,000

Work in process ? 185,000

Finished goods 65,000 115,000

During July, the cost of materials purchased was $160,000 and factory overhead of $125,000 was applied at a rate of 75% of direct labor cost. July cost of goods sold was $240,000.

Required: Prepare completed T accounts showing the flow of the cost of goods manufactured and sold.

SOLUTION

Materials Work in Process

Purch. 160,000 | Materials 135,000 |

180,000 | Factory |

45,000 | overhd. 125,000 |

| Labor 166,667 |

| 475,000 |

| 185,000 |

Finished Goods Cost of Goods Sold

WIP 290,000* | |

355,000 | |

115,000 | |

CGA-Canada (adapted). Reprinted with permission.

*Beginning inventory + WIP = Ending inventory + CGS

$65,000 + WIP = $115,000 + $240,000

WIP = $290,000

**Beginning WIP + Mfg. costs = Ending WIP + FG

Beginning WIP + $426,667 = $185,000 + $290,000

Beginning WIP = $48,333

I saw comments from people who already got their loan from Mr Pedro and I decided to apply under their recommendations and just 5 days later I confirmed my loan in my bank account a total amount of $850,000 .00 which I requested for.This is really a great news and I am advising everyone who needs real loan lender to apply through their email : pedroloanss@gmail.com or WhatsApp : +18632310632. I am happy now that I have gotten the loan I requested .

ReplyDelete