D 1. Expenses that require a series of payments over a long period of timeCsuch as long-term debt and lease rentalsCare frequently known as:

A. programmed fixed expenses

B. avoidable expenses

C. variable expenses

D. committed fixed expenses

E. normal capacity expenses

C 2. A mathematical technique used to fit a straight line to a set of plotted points is:

A. integral calculus

B. the EOQ model

C. the method of least squares

D. linear programming

E. PERT network analysis

E 3. One advantage of using multiple regression analysis is that:

A. computations are simplified

B. only two data points need be considered

C. a twodimensional graph may be used to show cost relationships

D. costs may be grouped into one independent variable

E. the effects of several variables on costs may be analyzed

B 4. The coefficient of determination indicates:

A. causal relationships among costs and other factors

B. the percentage of explained variance in the dependent variable

C. the linear relationship between two variables

D. whether several variables fluctuate

E. the size of the standard deviation

E 5. Hoyden Co. developed the following equation to predict certain components of its budget for the coming period:

Costs = $50,000 + ($5 x direct labor hours)

The $5 would approximate:

A. total cost

B. direct labor rate per hour

C. fixed cost per direct labor hour

D. the coefficient of determination

E. variable costs per direct labor hour

E 6. When cost relationships are linear, total variable manufacturing costs will vary in proportion to changes in:

A. machine hours

B. direct labor hours

C. total material cost

D. total overhead cost

E. volume of production

B 7. The term "relevant range" as used in cost accounting means the range over which:

A. relevant costs are incurred

B. cost relationships are valid

C. costs may fluctuate

D. sales volume fluctuates

E. production may vary

E 8. Within a relevant range, the amount of fixed cost per unit:

A. differs at each production level on a perunit basis

B. remains constant in total

C. decreases as production increases on a perunit basis

D. increases as production decreases on a perunit basis

E. all of the above

C 9. The following relationships pertain to a year's budgeted activity for Buckeye Company:

High Low

Direct labor hours 400,000 300,000

Total costs $154,000 $129,000

What are the budgeted fixed costs for the year?

A. $100,000

B. $25,000

C. $54,000

D. $75,000

E. none of the above

SUPPORTING CALCULATION:

High $ 154,000 400,000

Low 129,000 300,000

Difference $ 25,000 100,000

Variable rate = $25,000 100,000 = $.25/direct labor hour

Fixed cost = $154,000 - $.25(400,000) = $54,000

B 10. Maintenance expenses of a company are to be analyzed for purposes of constructing a flexible budget. Examination of past records disclosed the following costs and volume measures:

High Low

Cost per month $39,200 $32,000

Machine hours 24,000 15,000

Using the highlow method of analysis, the estimated variable cost per machine hour is:

A. $12.50

B. $0.80

C. $0.08

D. $1.25

E. none of the above

SUPPORTING CALCULATION:

High $ 39,200 24,000

Low 32,000 15,000

Difference $ 7,200 9,000

Variable rate = $7,200 9,000 = $.80/machine hour

D 11. A company allocates its variable factory overhead based on direct labor hours. During the past three months, the actual direct labor hours and the total factory overhead allocated were as follows:

October November December

Direct labor hours 2,500 3,000 5,000

Total factory

overhead allocated $80,000 $75,000 $100,000

Based upon this information, the estimated variable cost per direct labor hour was:

A. $.125

B. $12.50

C. $.08

D. $8

E. none of the above

SUPPORTING CALCULATION:

High $ 100,000 5,000

Low 80,000 2,500

Difference $ 20,000 2,500

Variable rate = $20,000 2,500 = $8.00/direct labor hour

A 12. The technique that can be used to determine the variable and fixed portions of a company's costs is:

A. scattergraph method

B. poisson analysis

C. linear programming

D. game theory

E. queuing theory

A 13. The number of variables used in simple regression analysis is:

A. two

B. three

C. more than three

D. three or less

E. one

C 14. Multiple regression analysis:

A. is not a sampling technique

B. involves the use of independent variables only

C. assumes that the independent variables are not correlated

D. establishes a causeandeffect relationship

E. all of the above

E 15. For a simple regression-analysis model that is used to allocate factory overhead, an internal auditor finds that the intersection of the line of best fit for the overhead allocation on the y-axis is $50,000. The slope of the trend line is .20. The independent variable, factory wages, amounts to $900,000 for the month. What is the estimated amount of factory overhead to be allocated for the month?

A. $910,000

B. $950,000

C. $ 50,000

D. $180,000

E. $230,000

SUPPORTING CALCULATION:

Factory overhead = $50,000 + .2($900,000) = $230,000

A 16. As a result of analyzing the relationship of total factory overhead to changes in machine hours, the following relationship was found:

y bar = $1,000 + $2 x bar

This equation was probably found by using the mathematical techniques called:

A. simple regression analysis

B. dynamic programming

C. linear programming

D. multiple regression analysis

E. none of the above

A 17. As a result of analyzing the relationship of total factory overhead to changes in machine hours, the following relationship was found:

y bar = $1,000 + $2 x bar

The y bar in the equation is an estimate of:

A. total factory overhead

B. total fixed costs

C. total machine costs

D. total variable costs

E. none of the above

C 18. As a result of analyzing the relationship of total factory overhead to changes in machine hours, the following relationship was found:

y bar = $1,000 + $2 x bar

The $2 in the equation is an estimate of:

A. fixed costs per machine hour

B. total fixed costs

C. variable costs per machine hour

D. total variable costs

E. none of the above

D 19. As a result of analyzing the relationship of total factory overhead to changes in machine hours, the following relationship was found:

y bar = $1,000 + $2 x bar

The use of such a relationship of total factory overhead to changes in machine hours is said to be valid only within the relevant range, which means:

A. within the range of reasonableness as judged by the department supervisor

B. within the budget allowance for overhead

C. within a reasonable dollar amount for machine costs

D. within the range of observations of the analysis

E. none of the above

C 20. A measure of the extent to which two variables are related linearly is referred to as:

A. sensitivity analysis

B. inputoutput analysis

C. coefficient of correlation

D. causeeffect ratio

E. costbenefit analysis

C 21. The appropriate range for the coefficient of correlation (r) is:

A. infinity r infinity

B. 0 r 1

C. 1 r 1

D. 100 r 100

E. none of the above

A 22. The covariation between two variables, such as direct labor hours and electricity expense, can best be measured by:

A. correlation analysis

B. simple regression analysis

C. multiple regression analysis

D. high-low method

E. scattergraph method

B 23. The quantitative method that will separate a semivariable cost into its fixed and variable components with the highest degree of precision is:

A. simplex method

B. least squares method

C. scattergraph method

D. account analysis

E. highlow method

A 24. If the coefficient of correlation between two variables is zero, a scatter diagram of these variables would appear as:

A. random points

B. a least squares line that slopes up to the right

C. a least squares line that slopes down to the right

D. under this condition, a scatter diagram could not be plotted on a graph

E. none of the above

D 25. Multiple regression analysis involves the use of:

Dependent Independent

Variables _ Variables

A. 1 none

B. 1> 1

C. 1> 1>

D. 1 1>

C 26. A company using regression analysis to correlate income to a variety of sales indicators found that the relationship between the number of sales managers in a territory and net income for the territory had a correlation coefficient of 1. The best description of this situation is:

A. that more sales managers should be hired

B. imperfect negative correlation

C. perfect inverse correlation

D. no correlation

E. perfect positive correlation

B 27. The correlation coefficient that indicates the weakest linear association between two variables is:

A. 0.73

B. 0.11

C. 0.12

D. 0.35

E. 0.72

B 28. If regression was applied to the data shown in Figure 3-1, the coefficients of correlation and determination would indicate the existence of a:

A. low linear relationship, high explained variation ratio

B. high inverse linear relationship, high explained variation ratio

C. high direct linear relationship, high explained variation ratio

D. high inverse linear relationship, low explained variation ratio

E. none of the above

A 29. Omitting important variables from the multiple regression is referred to as a(n):

A. specification error

B. autocorrelation

C. confidence loss

D. homoscedastic error

E. heteroscedastic error

E 30. When two or more independent variables are correlated with one another, the condition is referred to as:

A. serial correlation

B. autocorrelation

C. heteroscedacity

D. homoscedacity

E. multicollinearity

A 31. A large value for standard error of the estimate indicates that:

A. the actual cost will likely vary greatly from the estimated cost as portrayed by the regression line

B. the actual cost will be greater than the estimate cost as portrayed by the regression line

C. the actual cost will be less than the estimate cost as portrayed by the regression line

D. the actual cost will likely vary little from the estimated cost as portrayed by the regression line

E. none of the above

D 32. The confidence interval represents:

A. the percentage of variance in the dependent variable as explained by the independent variable

B. the measure of the extent to which variables are related linearly

C. the standard deviation about the regression line

D. a range of values within which the dependent variable is expected to fall a certain percentage of the time

E. none of the above

C 33. When the distribution of observations around the regression line is uniform for all values of the independent variable, it is:

A. heteroscedastic

B. serially correlated

C. homoscedastic

D. autocorrelated

E. none of the above

E 34. Expenses that are fixed at management's discretion at a certain level for the period are referred to as:

A. committed fixed costs

B. mixed costs

C. opportunity costs

D. sunk costs

E. programmed fixed costs

A 35. The separation of fixed and variable costs is necessary for all of the following purposes except:

A. absorption costing and net income analysis

B. direct costing and contribution margin analysis

C. break-even and cost-volume-profit analysis

D. differential and comparative cost analysis

E. capital budgeting analysis

PROBLEMS

PROBLEM

1.

High and Low Points Method. A controller is interested in analyzing the fixed and variable costs of indirect labor as related to direct labor hours. The following data have been accumulated:

Indirect Direct Labor

Month Labor Cost Hours

March $2,880 425

April 3,256 545

May 2,820 440

June 3,225 560

July 3,200 540

August 3,200 495

Required: Determine the amount of the fixed portion of indirect labor expense and the variable rate for indirect labor expense, using the high and low points method. (Round the variable rate to three decimal places and the fixed cost to the nearest whole dollar.)

SOLUTION

Indirect Direct Labor

Labor Cost Hours

High $ 3,225 560

Low 2,880 425

Difference $ 345 135

Variable rate = $345 135 = $2.556 per direct labor hour

Fixed cost = $3,225 ($2.556 x 560) = $1,794

PROBLEM

2.

Fixed, Variable, and Semivariable Production Costs. Ibus Instruments Co. developed the following regression equations to indicate costs at various activity levels:

Direct labor = $4 per unit

Materials = $3 per unit

Supervision = $5,000

Power = $300 + $.25 per unit + $.50 per machine hour

Factory supplies = $250 + $.75 per unit

DepreciationCequipment = $1 per machine hour

DepreciationCbuilding = $10,000

During the next period, the company anticipates production of 20,000 units and usage of 3,000 machine hours.

Required: Prepare a schedule of the production costs to be incurred during the next period.

SOLUTION

Production costs:

Direct labor $ 80,000

Direct materials 60,000

Overhead to be incurred:

Supervision $ 5,000

Power [$300 + ($.25 x 20,000 units) +

($.50 x 3,000 machine hours)] 6,800

Factory supplies [$250 + ($.75 x 20,000 units)] 15,250

DepreciationCequipment 3,000

DepreciationCbuilding 10,000 _ 40,050

Total production cost $ 180,050

PROBLEM

3.

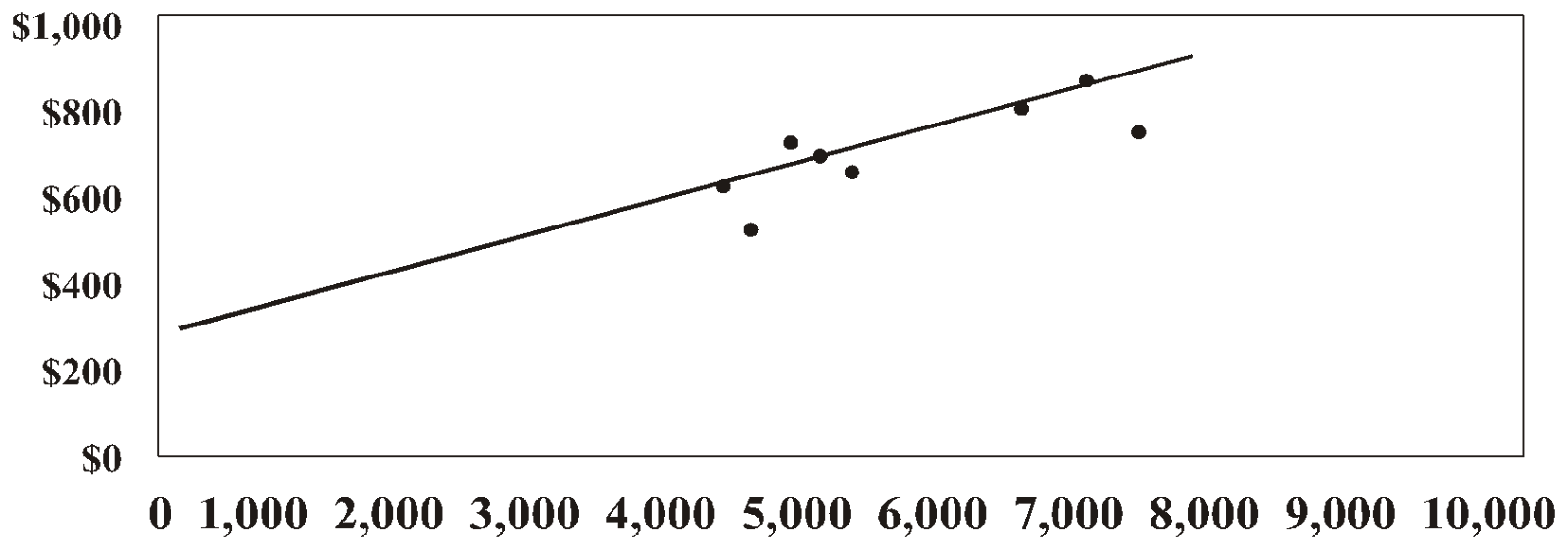

Statistical Scattergraph. Dale Company management is interested in determining the fixed and variable components of electricity expense, a semivariable cost, as measured against machine hours. Data for the first eight months of the current year follow:

Machine Electricity

Month Hours _ Cost

January 4,500 $650

February 4,750 600

March 5,000 750

April 5,500 700

May 7,250 900

June 7,500 800

July 6,750 825

August 5,250 725

Required: Graph the data provided and determine the total fixed cost and the variable cost per machine hour for electricity. (Round estimates to the nearest cent.)

SOLUTION

Average cost ($5,950 8) $743.75

Fixed cost per month (from graph) 200.00

Average total variable cost $543.75

PROBLEM

4.

Method of Least Squares. The management of Rainbow Inc. would like to separate the fixed and variable components of electricity as measured against machine hours in one of its plants. Data collected over the most recent six months follow:

Electricity Machine

Month Cost _ Hours

January $1,100 4,500

February 1,110 4,700

March 1,050 4,100

April 1,200 5,000

May 1,060 4,000

June 1,120 4,600

Required: Using the method of least squares, compute the fixed cost and the variable cost rate for electricity expense. (Round estimates to the nearest cent.)

SOLUTION

(1) (2) (3) (4) (5) (6)

Electricity Cost Machine Activity

Month Cost _ Deviation Hours _ Deviation (4) Squared (4) x (2)

January $1,100 (7) 4,500 17 289 (119)

February 1,110 3 4,700 217 47,089 651

March 1,050 (57) 4,100 (383) 146,689 21,831

April 1,200 93 5,000 517 267,289 48,081

May 1,060 (47) 4,000 (483) 233,289 22,701

June 1,120 13 _ 4,600 117 _ 13,689 1,521

$6,640 (2)* 26,900 2* 708,334 94,666

y bar = Σy n = $6,640 6 = $1,107

x bar = Σx n = $26,900 6 = $4,483

*rounding difference

Fixed cost = $1,107 - ($.13)(4,483) = $524.21

PROBLEM

5.

Coefficients of Correlation and Determination. The president of Scranton Steel Co. has prepared the following data so that an assessment may be made for developing a regression analysis of smelting costs:

Year Smelting Costs Direct Labor Hours Kilograms of Iron Smelted

19_1 $12,000 2,100 50.2

19_2 12,900 1,800 55.6

19_3 13,500 2,250 60.0

19_4 12,750 2,400 54.0

19_5 14,100 2,250 64.4

Total $65,250 10,800 284.2

Required: Compute the coefficient of correlation (r) and the coefficient of determination (r2) for each of the independent variables. (Round to three decimal places.)

Note to instructor: It may be helpful to provide students with the following equation:

SOLUTION

DIRECT LABOR HOURS

(1) (2) (3) (4) (5) (6) (7)

Difference Difference

from from

Average Direct Average

Smelting of Labor of 2,160

Costs _ $13,050 _ Hours _ Hours _ (4) Squared (4) x (2) (2) Squared

$12,000 (1,050) 2,100 (60) 3,600 63,000 1,102,500

12,900 (150) 1,800 (360) 129,600 54,000 22,500

13,500 450 2,250 90 8,100 40,500 202,500

12,750 (300) 2,400 240 57,600 (72,000) 90,000

14,100 1,050 2,250 90 8,100 94,500 1,102,500

$65,250 0 10,800 0 207,000 180,000 2,520,000

KILOGRAMS OF IRON SMELTED

(8) (9) (10) (11)

Difference

Kilograms of from Average

Iron Smelted of 56.84 _ (9) Squared (9) x (2)

50.2 (6.64) 44.0896 $6,972

55.6 (1.24) 1.5376 186

60.0 3.16 9.9856 1,422

54.0 (2.84) 8.0656 852

64.4 7.56 57.1536 7,938

284.2 0.00 120.8320 $17,370

PROBLEM

6.

Standard Error of the Estimate and Confidence Interval Estimation. The production supervisor of Lyle Inc. would like to know the range of electricity cost that should be expected about 95 percent of the time at the 15,000 direct labor hour level of activity. The least squares estimate of electricity cost at that level of activity is $750. The least squares parameter estimates (i.e., the estimates of fixed cost and the variable cost rate) were derived from a sample of data for a recent 12-month period. The direct labor hour average for the sample period is 13,000, and the direct labor hour deviations from its average squared and summed (Σ(xi-xi)2) is 80,000,000. The prediction error squared (Σ(yi-yi)2) over the sample period is $40,850.

Required:

Compute:

(1) the standard error of the estimate

(2) the 95 percent confidence interval (Table factor 2.228) estimate for electricity cost at the 15,000 direct labor hour level of activity

(Round answers to the nearest whole dollar.)

SOLUTION

(1)

(2)

PROBLEM

7.

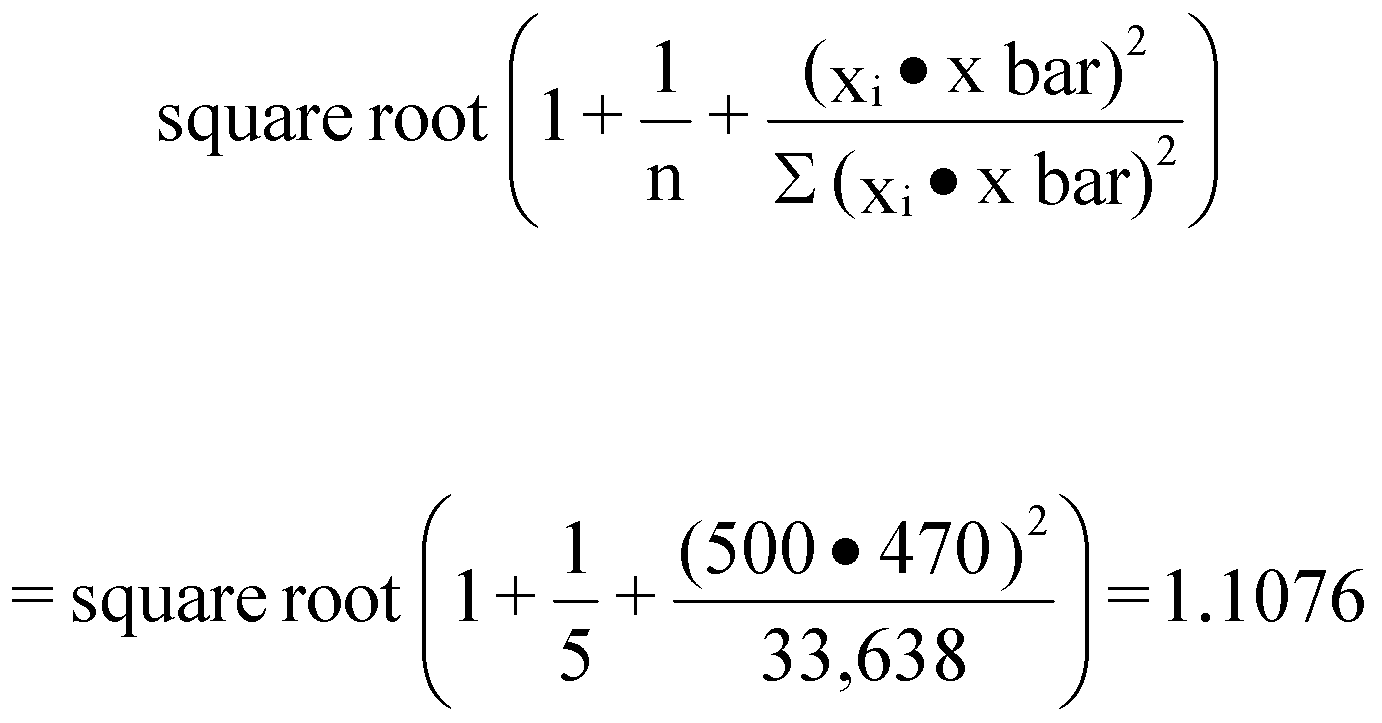

Method of Least Squares. The data below are found to be highly correlated for Mystic Modem Manufacturing Corp.:

Fabricating Kilograms of

Costs _ Materials Used

$15,600 360

18,000 463

17,100 412

21,300 595

19,500 520

$91,500 2,350

Required:

(1) Write an equation reflecting the relationship between fabricating costs and kilograms of materials used, using the method of least squares.

(2) Determine the standard error of the estimate.

(3) Determine the standard error of the estimate correction factor when direct labor hours are 500.

(4) Determine the coefficient of correlation (r) and the coefficient of determination (r2).

(Round dollar amounts to the nearest cent and unit amounts to four decimal places.)

SOLUTION

(1)

(1) (2) (3) (4) (5) (6) (7)

Difference

from Difference

Average Kilograms from

Fabricating of of Materials Average of

Costs _ $18,300 _ Used _ 470 _ (4) Squared (4) x (2) (2) Squared

$15,600 (2,700) 360 (110) 12,100 $297,000 $ 7,290,000

18,000 (300) 463 (7) 49 2,100 90,000

17,100 (1,200) 412 (58) 3,364 69,600 1,440,000

21,300 3,000 595 125 15,625 375,000 9,000,000

19,500 1,200 520 50 _ 2,500 60,000 1,440,000

$91,500 0 2,350 0 _ 33,638 $803,700 $19,260,000

y = a + bx

$18,300 = a + ($23.89 x 470)

a = $18,300 $11,228.30

a = $7,071.70

Equation: y = $7,071.70 + $23.89x

(2)

(1) (2) (3) (4) (5)

Kilograms of Prediction Prediction

Materials Fabricating Predicted Error Error Squared

Used Costs _ Fabricating Costs (2) (3) (4) Squared

360 $15,600 $15,672 $ (72) $ 5,184

463 18,000 18,133 (133) 17,689

412 17,100 16,914 186 34,596

595 21,300 21,286 14 196

520 19,500 19,495 5 25

2,350 $91,500 $91,500 $ 0 $57,690

(3)

(4)

No comments:

Post a Comment